Active Asset Test vs Passive Asset Rules

Active Asset Test vs Passive Asset Rules

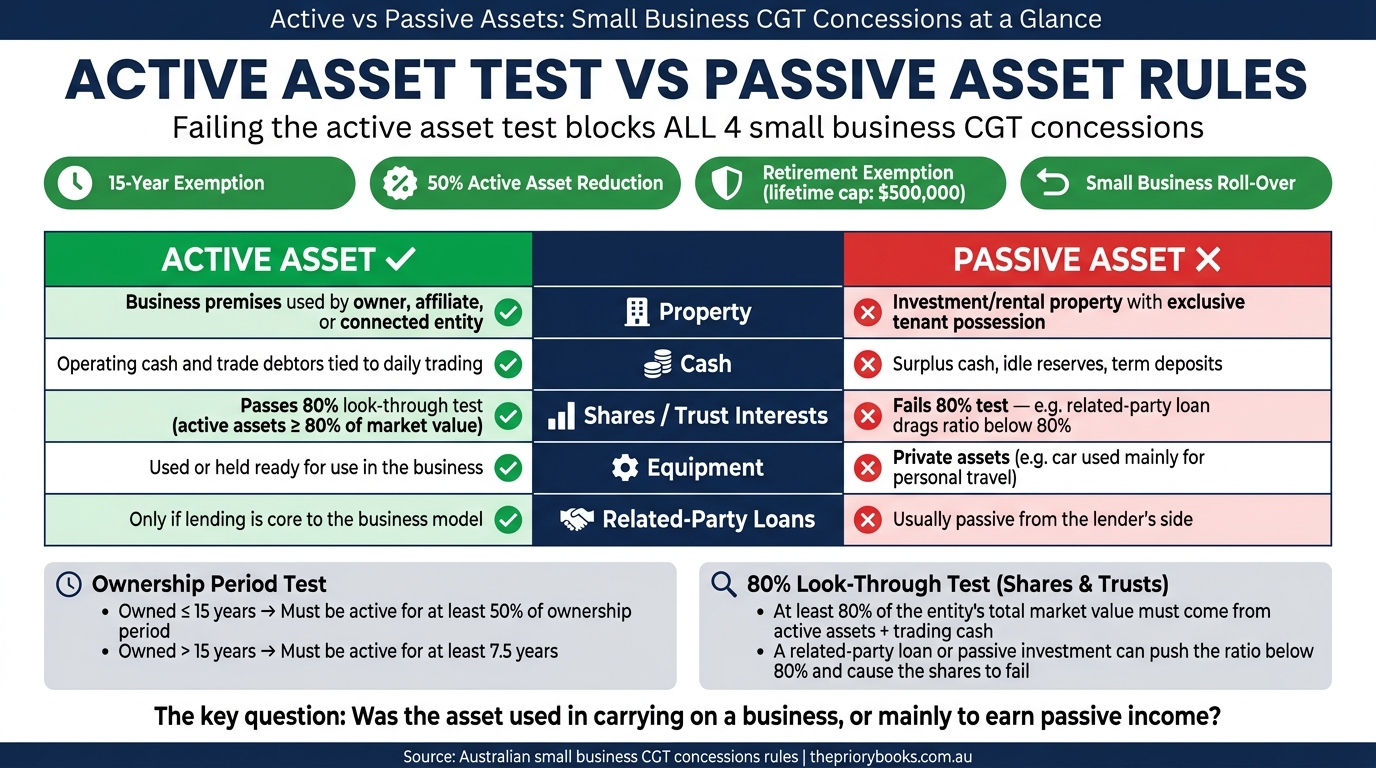

If your asset is used mainly to earn rent, interest, royalties, annuities, or foreign exchange gains, it will usually miss the active asset test - and that can block all 4 small business CGT concessions.

When I look at this issue, I keep it simple: how the asset was used matters more than what the asset is called. For CGT, a business premises, working cash balance, or equipment item may qualify. A rental property, idle cash reserve, related-party loan, or passive investment often will not.

Here’s the short version:

- Property: business use may pass; rental use usually fails.

- Cash: day-to-day trading cash may pass; surplus cash usually fails.

- Shares and trust interests: they are tested by looking through to the entity’s assets.

- Equipment: assets used, or held ready for use, in the business will usually pass.

- Timing rule:

- owned for 15 years or less → active for at least 50% of that time

- owned for more than 15 years → active for at least 7.5 years

- Look-through rule for shares/trust interests: at least 80% of the entity’s market value must come from active assets and trading cash.

If an asset fails the active asset test, you will usually miss out on:

- the 15-year exemption

- the 50% active asset reduction

- the retirement exemption

- the small business roll-over

The core question is simple: was the asset used in carrying on a business, or was it used mainly to earn passive income? That is the line this guide focuses on.

Active vs Passive Assets: Small Business CGT Concessions at a Glance

Active Asset Test | Shares & Trusts

sbb-itb-98a37a2

Quick Comparison

| Asset | Usual tax treatment | What decides it | Small business CGT concessions? |

|---|---|---|---|

| Business premises | Active | Used in the business by you, an affiliate, or a connected entity | Usually yes |

| Investment property | Passive | Main use is earning rent, often with exclusive possession | Usually no |

| Working cash / trade debtors | Can be active | Must be tied to day-to-day business needs | Sometimes |

| Surplus cash / idle reserves | Passive | Not tied closely enough to business use | Usually no |

| Shares / trust interests | Can be active | Must satisfy the 80% look-through test | Sometimes |

| Business equipment | Active | Used or held ready for use in the business | Usually yes |

| Private assets | Passive | Main use is private, not business | No |

So before any sale, I would check use, income source, ownership period, and records first. That gives you a clearer view of whether the gain may qualify for the small business CGT concessions.

2. Investment property vs business premises

When property is usually a passive asset

Property usually comes down to two things: who has possession and who gets the income.

If a property is mainly used to earn rent, it's usually treated as passive. That means it will usually fail the active asset test. The big issue is exclusive possession. If a tenant has the right to occupy the space under a lease, the income is usually rent, and the property will usually fail the test. A standard residential rental is the clearest example.

If the owner later sells, they may still get the general 50% CGT discount if they have held the property for more than 12 months. But the extra small business CGT concessions - the 15-year exemption, the 50% active asset reduction, and the retirement exemption - will usually not be available.

That said, the same property can move into active-asset territory if it's used in a business instead of being leased to outside tenants.

When property can still be an active asset

A shop, office, warehouse, or manufacturing plant is different when it's being used in a business. If the owner, an affiliate, or a connected entity uses the premises for business operations, rather than leasing it to a third-party tenant, the property is being used in the business and will generally pass the active asset test.

The rules also cover property leased to a connected entity or affiliate. The ATO example of Palik shows how this works. Palik owned land and leased it to Fossy Farm Pty Ltd, a company she wholly owned. Even though Palik did not run a business herself, the land still qualified as an active asset because it was used in the business of a connected entity that met the small business turnover threshold.

Mixed-use property sits in a grey area. The ATO looks at:

- area

- time

- income

In practice, income usually carries the most weight.

There's another wrinkle here. If the owner provides real services and guests do not have exclusive possession, the property can shift from passive to active. In plain English, it starts looking less like simple rent and more like business income.

Comparison table: rental property vs trading premises

| Feature | Investment/Rental Property | Trading/Business Premises |

|---|---|---|

| Main use | Deriving passive rental income from third parties | Used in day-to-day business operations |

| Who controls the space | Tenant usually has exclusive possession | Owner or connected entity uses the space for trade |

| Active asset status | Generally fails (passive) | Generally passes (active) |

| Key exceptions | May be active if used by a connected entity or affiliate in a business. | May fail if the rented-out part dominates area and income. |

| CGT result | Usually only the general CGT discount | May access small business CGT concessions |

Once property is sorted, the next issue is whether assets like cash, loans, and shares can still count as active assets. Here, the line between active and passive gets tighter again.

3. Surplus cash and shares: where passive asset rules matter most

Working cash vs surplus cash reserves

After property, the next big trouble spots are cash, loans and shareholdings. These assets are harder to assess because the test looks at how the money is used, not just where it sits.

Operating cash, trade debtors and cash held for day-to-day trading will usually count as active. By contrast, idle reserves, term deposits, bonds and unrelated loans usually will not.

Related-party loans are a common snag. If lending is not part of the business model, a loan from one entity to a connected entity is usually treated as passive from the lender's side.

How shares and trust interests are tested

Shares and trust interests are tested by looking through to the assets inside the entity. In plain terms, you do not stop at the share certificate or trust interest itself. You look at what sits underneath it.

Under this look-through test, the market value of the entity's active assets, plus any cash needed for day-to-day trading, must make up at least 80% of the total market value of all its assets.

That 80% line matters a lot. Passive assets can drag the entity below it. Archimedes Pty Ltd shows how this can happen: a related-party loan brought the active asset ratio down to 70%, so the shares failed the test.

That said, not every dip below 80% is fatal. A short, event-driven drop may still be accepted, as the Fruit and Veg Co example shows.

Comparison table: cash, loans and shares

| Asset Type | Usual result | What changes it | Effect on Small Business CGT Concessions |

|---|---|---|---|

| Operating cash / trade debtors | Active | Must be needed for day-to-day trading | Counts towards the 80% threshold |

| Surplus / idle cash | Passive | Only active if held because of a temporary trading spike or the recent sale of a business asset | Can push the entity below the 80% threshold |

| Related-party loans | Passive | Rarely active; must be part of the business model | Often excluded from the active asset calculation |

| Investment shares | Passive | Generally excluded from active asset status | Usually do not qualify for small business CGT concessions |

| Shares in a trading company | Active, if the underlying entity passes the 80% test | May qualify if the underlying entity passes the 80% test | May qualify for small business CGT concessions |

Physical business assets are a bit more straightforward. The next section looks at why equipment will usually pass, while private assets usually will not.

4. Business equipment vs private or non-business assets

Equipment, plant and fit-out are usually active assets

Unlike cash and shares, business equipment is usually more straightforward. Machinery, tools, furniture, plant and fit-outs are generally active assets if they are used, or held ready for use, in the course of carrying on a business.

That "held ready for use" point matters. A machine sitting in storage and ready for opening can still be active. By contrast, materials kept aside for some undefined future project are not. Equipment can also remain active if an affiliate or a connected entity uses it in their business.

Private assets do not get the same treatment

Private assets don't qualify. A car used mainly for personal travel stays passive, even if you sometimes use it to visit clients. In plain terms, the business-versus-private split is what decides whether an asset falls on the active or passive side of the test.

Before a sale, check depreciation. Most business equipment is a depreciating asset, so selling it may trigger a balancing adjustment. The balancing adjustment is ordinary income, not a CGT gain.

Before a sale, test each asset separately.

5. Putting the rules together before selling an asset

Once you’ve looked at each asset on its own, the next step is to pull the rules together before any sale.

Asset-by-asset summary

Before selling, check each asset against three things: how it was used, where the income came from, and who owned it over time. The point isn’t the name of the asset. What matters is whether it was used in a business or used mainly to earn passive income.

The table below gives a quick view of the usual CGT outcome.

Comparison table: which assets usually qualify for the small business CGT concessions

| Asset Type | Usually Active or Passive | Key test | Usually eligible? |

|---|---|---|---|

| Business Premises | Active | Used by the owner, affiliate, or connected entity and satisfies the timing rule | Usually |

| Investment Property | Passive | Main use is to derive rent; exclusive possession points to a rental arrangement | Only if rental use was only temporary |

| Business Equipment | Active | Used or held ready for use in carrying on the business | Usually |

| Trade Debtors / Working Cash | Conditional | Must be inherently connected to business operations | Only if genuinely connected |

| Surplus Cash / Loans | Passive | Usually not inherently connected to daily business | No |

| Shares / Trust Interests | Conditional | Must pass the 80% market value test | Only if the 80% test is met |

| Private Assets | Passive | Personal use by the owner or affiliate | No |

Once you’ve pinned down the asset type, the next job is to prove how it was used with proper records.

Key points and record-keeping before a sale

Asset status turns on use, not label. The ATO treats assets mainly used to earn rent, interest, annuities, royalties, or foreign exchange gains as passive.

This is where records matter. A lot. You’ll want usage logs, lease agreements, financial statements that split business income from passive income, and a clear register of affiliated and connected entities. If shares are involved, get a market value breakdown of the underlying entity’s assets before any sale. Clean bookkeeping and tax records, including through The Priory Books and Tax, help show the position before sale.

Miss the active asset test and all four small business CGT concessions are off the table: the 15-year exemption, the 50% active asset reduction, the retirement exemption, and rollover relief. The retirement exemption has a lifetime cap of $500,000. Test each asset on its own and keep full ownership records before sale.

FAQs

Can a mixed-use property still qualify?

Yes - if it meets the active asset test.

Look at the property as a whole, not just the part used for business.

If a significant part of the property is used in a business carried on by you, an affiliate, or a connected entity, it may qualify.

But if the property’s main use is to earn rent from unrelated third parties, it generally won’t qualify.

How do I prove cash is for business use?

You need to show that the cash is tied to your day-to-day business operations. Interest-bearing investments are usually passive, but cash can count as an active asset when it comes from trade debtors or recent sales and is being held for business use.

Keep clear records that connect the cash to active business activities, not long-term investment aims.

What happens if shares fail the 80% test?

If shares or units fail the 80% test, they are not treated as active assets for the small business CGT concessions.

And that has a big flow-on effect. You can't use those concessions, including the 15-year exemption, 50% reduction, retirement exemption and rollover.

This usually happens when a company holds a large amount of passive investments, such as rental properties. If those passive assets make up more than 20% of the company's total market value, the shares or units won't meet the test.