Medicare Levy Surcharge for Sole Traders

Medicare Levy Surcharge for Sole Traders

If you’re a sole trader, the Medicare Levy Surcharge can hit even when your business profit looks modest. I’d check three things before 30 June: your MLS income, your private hospital cover, and your family status for each day of the year.

Here’s the short version:

- The Medicare levy is usually 2% of taxable income

- The MLS is an extra 1%, 1.25% or 1.5%

- For 2025–26, MLS starts above $101,000 for singles and $202,000 for families

- Your MLS income is not just sole trader profit

- It can include reportable super contributions, reportable fringe benefits, and net investment losses

- Extras-only cover does not stop MLS

- MLS is worked out day by day, so part-year cover gaps can still lead to a charge

- If you have a spouse or dependants, the family threshold may apply, and all family members usually need eligible hospital cover

What catches people out is simple: cash in the bank, turnover, and taxable income are not the same as MLS income. I’d treat this as a personal tax issue, not a business-only one, and line up your income figures, insurer statement, and family details before lodging.

This article walks through the main checks so you can spot a surcharge risk early and fix errors before they turn into an amended assessment.

What is the Medicare Levy & Surcharge? (Explained For Australians)

sbb-itb-98a37a2

Medicare levy vs Medicare Levy Surcharge: what sole traders need to know

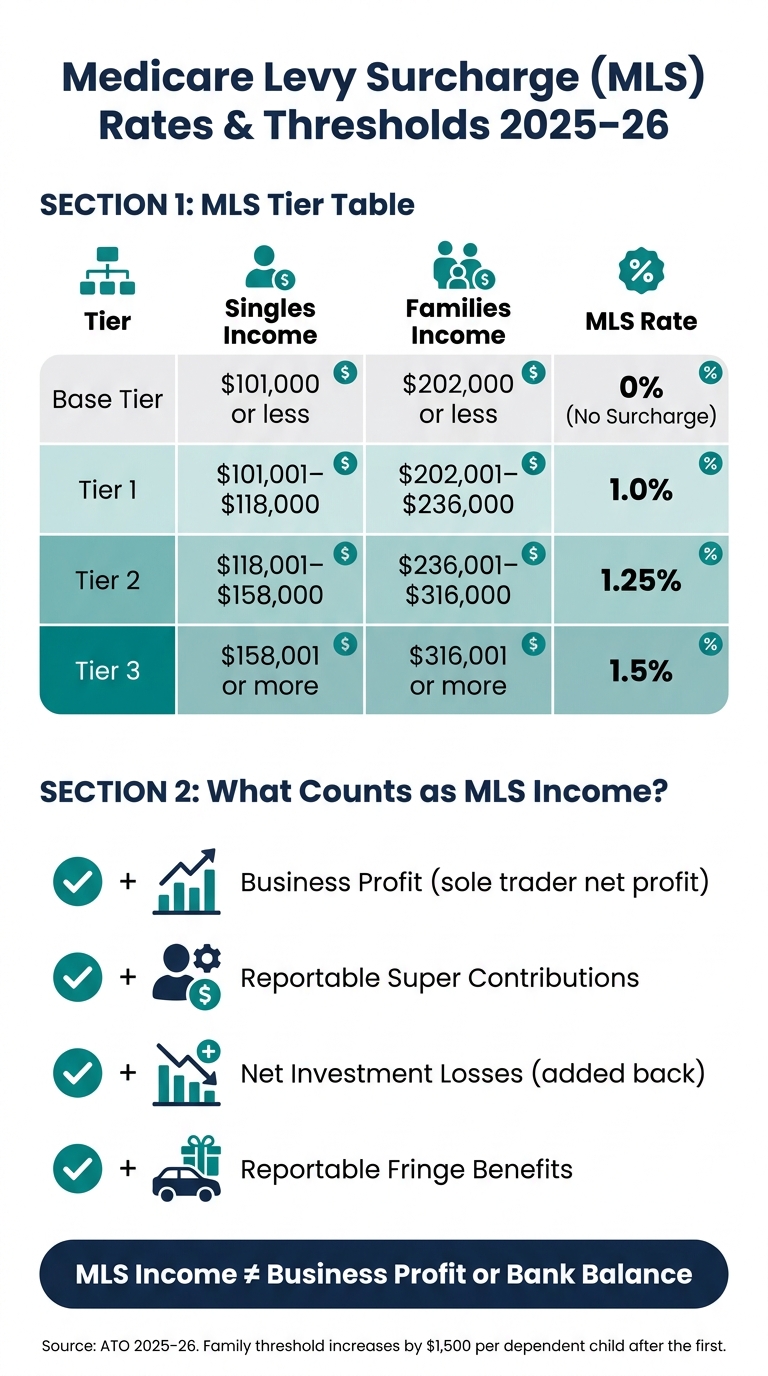

Medicare Levy Surcharge Rates & Thresholds 2025–26

The Medicare levy is usually 2% of your taxable income. The Medicare Levy Surcharge (MLS) is a separate extra tax that can apply if your MLS income is over the threshold and you don’t have eligible private hospital cover.

For sole traders, this is where people often come unstuck: your business profit doesn’t sit in its own tax bucket.

Problem: Thinking business income is assessed separately from personal tax

It’s easy to assume the MLS works like a business cost or a separate tax tied only to your sole trader income. It doesn’t.

Both the Medicare levy and the MLS are worked out in your individual tax return. That means your business profit is added to other MLS income, such as interest and dividends.

If you’re a sole trader, you’ll usually get business income without tax being withheld, so it makes sense to put money aside during the year.

Solution: Check the correct MLS threshold and rate before lodging

Before you lodge, work out your MLS income - not just your net business profit. That small detail can make a big difference.

If you have a spouse, the test uses your combined family income against the family tiers, even if your own income is below the single threshold.

The MLS rates and thresholds for 2025–26 are:

| Tier | Singles Income | Families Income | MLS Rate |

|---|---|---|---|

| Base Tier | $101,000 or less | $202,000 or less | 0% |

| Tier 1 | $101,001 – $118,000 | $202,001 – $236,000 | 1.0% |

| Tier 2 | $118,001 – $158,000 | $236,001 – $316,000 | 1.25% |

| Tier 3 | $158,001 or more | $316,001 or more | 1.5% |

Before lodging, add up:

- taxable income

- reportable fringe benefits

- reportable super contributions

- net investment losses

Next, check which income items and cover details change whether the surcharge applies.

How sole trader income can push you over the MLS threshold

Most sole trader surprises come down to three things: higher profit, rental losses, or super contributions. And here’s the bit that catches people out: the ATO looks at MLS income, not your bank balance or total sales.

That matters because income for MLS purposes can be higher than taxable income.

Why? Because of the add-backs. Some amounts that lower your taxable income, such as deductible personal super contributions or rental property losses, get added back when the ATO works out your MLS income. So if you're a sole trader who tips extra into super or negatively gears a property, you could still land well above the threshold when the surcharge is worked out.

| Income type | Counted in MLS income | Common sole trader issue |

|---|---|---|

| Business Profit | Yes | Confusing gross turnover with net taxable profit |

| Reportable Super Contributions | Yes | Assuming personal deductible super contributions lower the MLS bracket |

| Net Investment Losses | Yes | Thinking a rental property loss reduces MLS income |

| Reportable Fringe Benefits | Yes | Overlooking non-cash benefits from another role or business |

Problem: Looking only at sales or cash in the bank

Turnover is not profit, and profit is not MLS income.

So even if you brought in $180,000 in sales, your MLS income can still sit above the threshold once business profit, super contributions, and rental losses are factored back in. That’s where people get tripped up. The cash in your account might tell one story, but the ATO’s MLS test tells another.

Solution: Use accurate profit figures and include all personal income sources

Start with a fully reconciled profit figure from your accounting records. If transactions are uncoded or expenses are missed, your taxable income can look higher than it should. It’s much easier to sort that out before 30 June than to rush through it at lodgement time.

Then work through the add-backs. Include any deductible super contributions, check for reportable fringe benefits, and factor in net investment losses. myTax works out your final MLS income figure in the Income Tests section, so it’s worth checking that screen before you lodge if you want to avoid a nasty surprise.

Once you’ve got the right MLS income figure, the next step is checking whether your private hospital cover removes the surcharge.

How private health cover and family status affect your MLS outcome

Once you’ve confirmed your MLS income, the next thing to check is your hospital cover. This is where people often get caught out.

MLS is worked out day by day, so the surcharge can apply for each day you didn’t have an eligible policy. And not just any policy counts. The excess has to be $750 or less for singles or $1,500 or less for couples and families. If your policy excess is above those limits, it won’t exempt you from MLS.

Problem: Assuming any health insurance policy will avoid MLS

A lot of people see “private health insurance” and assume they’re in the clear. Not always.

An extras-only policy won’t remove the surcharge. A hospital policy with an excess above the MLS limit won’t remove it either. And if you only had eligible hospital cover for part of the year, you can still be charged MLS for the days you weren’t covered.

That’s why the next step isn’t just checking if you had cover. It’s checking what type of cover you had, who it covered, and for how many days.

Solution: Match your cover details to your family situation and days covered

Your family status affects the income threshold that applies to you. If your status changed during the year, the rules follow those dates. The single threshold applies for the days you were single, and the family threshold applies for the days you had a spouse or dependants.

There’s another detail here: the family threshold goes up by $1,500 for each dependent child after the first. And if you’re a single parent, you use the family threshold.

For families, the cover test is stricter than many people expect. To avoid the surcharge, you, your spouse, and all dependants must have eligible hospital cover. If even one dependant isn’t covered, MLS may still apply. That’s why it’s smart to add a newborn to the policy straight away, because the surcharge is worked out from the day they become a dependant.

Before you lodge, pull out your annual private health insurance statement and line it up against the days you were covered. It’s the simplest way to spot a gap before the ATO does.

Records that prevent MLS errors and steps to fix past mistakes

Even if your cover looks right, the ATO still checks your return against insurer data and income records. If those records don’t line up, you can end up with an amended assessment and an MLS bill you didn’t see coming.

After you’ve checked your threshold and cover, the last big risk is mismatched records. These four records deal with the main MLS trouble spots: wrong income, wrong cover days, and wrong family status.

| Record | How it affects MLS | What can go wrong if missing | Best place to check it |

|---|---|---|---|

| Xero profit and loss report | Determines the business profit part of your MLS income, backed by a reconciled bank feed | Unreconciled transactions or miscoded expenses can produce incorrect profit figures and put you in the wrong MLS tier | Xero Reports > Profit and Loss |

| Private health insurance statement | Confirms the exact days you held eligible cover | Missing days of cover can leave your MLS calculation wrong | Your health insurer's online member portal |

| Spouse Notice of Assessment or income statement | Combined income determines whether the family threshold applies | Using the single threshold when the family threshold applies can lead to the wrong calculation | Spouse's Notice of Assessment or income statement |

| Reportable super contributions and fringe benefits | These amounts are added back to your income for MLS purposes | Missing these add-backs can leave your MLS calculation wrong | ATO myGov income statement or super fund records |

Solution: Keep clean Xero records and health cover documents during the year

The easiest way to avoid MLS mistakes is to keep your records in order during the year instead of trying to sort it all out in June or July. Reconcile your bank transactions in Xero each month so your profit and loss report matches your actual business profit. It sounds basic, but it matters. If expenses are coded to the wrong account, your profit can look too high or too low, and that can flow straight into your MLS result.

After 30 June, download your annual private health insurance statement from your insurer’s member portal as soon as it’s ready. That statement shows the exact number of days you had eligible cover, and that’s what the ATO uses when working out any pro-rata surcharge. Save it with the rest of your tax records for that year so it’s easy to find later.

Solution: Fix past errors and plan ahead with registered tax support

If what you lodged doesn’t match the ATO’s data, deal with it early. If you’ve already lodged and spot a problem - maybe the cover days were wrong, the income figure was off, or your family status wasn’t reported properly - you can amend your return. Online amendments through ATO online services take about 20 business days to process. A registered tax agent can also help with the amendment.

If you get an ATO data-matching letter or a Notice of Assessment with a surcharge you weren’t expecting, check the lodged figures against your private health insurance statement and your Xero profit and loss report. That side-by-side check often shows where things went off track. And if your business profit is climbing each year, keep an eye on your MLS position as part of your yearly tax review. Going over a threshold by just $1 can trigger the surcharge on your income for the days you were uninsured.

If your records need a clean-up before lodging, The Priory Books and Tax can help. The Priory Books and Tax helps sole traders keep Xero records clean and lodge tax returns through a secure client portal.

Conclusion: Key checks to avoid a surcharge surprise at tax time

The Medicare levy and MLS are not the same thing. For sole traders, the main trap is simple: missing one of these three checks - income, cover, or timing.

Before you lodge, check your MLS income, not just your business profit. That means using your business profit plus all personal add-backs, including reportable super contributions, reportable fringe benefits, and net investment losses, to test whether MLS applies.

Then check your health cover. Your policy needs to be hospital cover, the excess must sit within the MLS limit, and the cover dates need to line up with your insurer statement. If your cover started partway through the financial year, the surcharge is worked out day by day.

Before lodging, compare your Xero profit and loss report, private health statement, and family income for MLS purposes against the MLS test.

FAQs

How do I work out my MLS income?

For Medicare Levy Surcharge purposes, your income is more than just your taxable income.

The ATO also adds back:

- reportable fringe benefits

- total net investment losses, such as negative gearing

- reportable super contributions

If you have a spouse, the ATO looks at your combined income when checking whether you’re over the MLS threshold.

Does part-year hospital cover still trigger MLS?

Yes. The Medicare Levy Surcharge (MLS) is calculated day by day across the financial year.

That means if you don't have the right level of private patient hospital cover for every day of the year, you may still need to pay MLS for the days you weren't covered.

If you take out cover partway through the year, it only stops MLS from applying from that date onward.

What if my family situation changed during the year?

If your family situation changed during the financial year, the Medicare levy surcharge is worked out based on each period when you were:

- single

- with a spouse

- with dependent children

The ATO applies the right threshold to your income for each of those periods.

That means even a change partway through the year can affect how the surcharge is worked out. Priory Books and Tax can help you keep your records in order and make sure your tax lodgement reflects those changes properly.