ATO Home Office Claim Methods: Comparison

ATO Home Office Claim Methods: Comparison

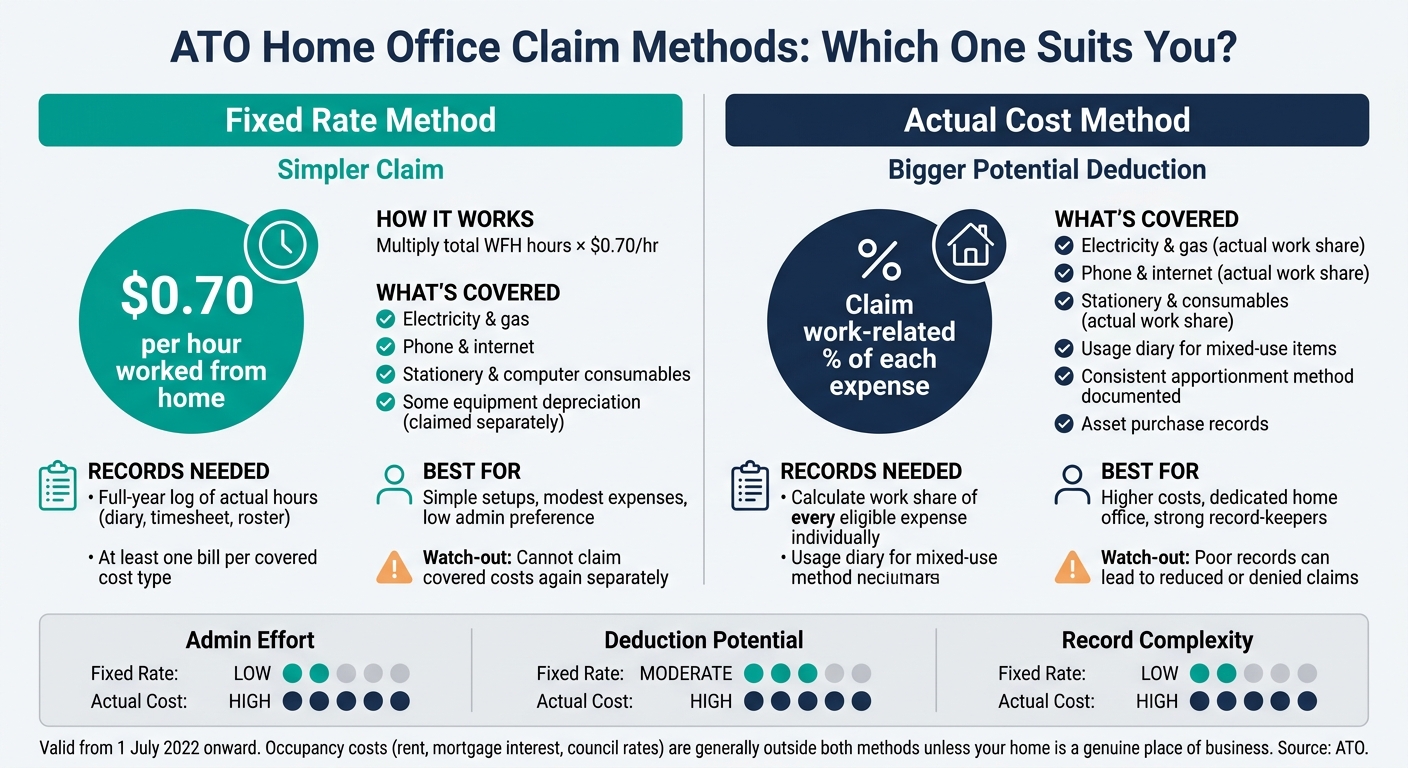

If you work from home in Australia, the main choice for 2025–26 is simple: claim $0.70 per hour under the fixed rate method, or claim the work share of each cost under the actual cost method.

I’d sum it up like this: the fixed rate method is easier, while the actual cost method can give a bigger deduction if your home office costs are high and your records are solid. The main test is not just what you spent, but what you can prove.

Here’s the short version:

- Fixed rate method: claim $0.70 per work-from-home hour

- Actual cost method: claim each work-related expense separately

- Fixed rate covers: electricity, phone, internet, stationery, and computer consumables

- Actual cost needs: receipts, invoices, and a clear work/private split

- Occupancy costs like rent, mortgage interest, and council rates are usually outside both methods unless your home is a genuine place of business

- Since 1 July 2022, fixed rate claims need a record of actual hours for the full income year

My takeaway: if your setup is plain and your admin needs to stay low, fixed rate will often do the job. If you have higher power use, higher internet use, or equipment costs, actual cost may be worth the extra paperwork.

How to Calculate Your Work‑From‑Home Actual Cost Deduction (ATO Step‑By‑Step Guide)

sbb-itb-98a37a2

Quick Comparison

ATO Home Office Claim Methods: Fixed Rate vs Actual Cost (2025–26)

| Method | How it works | What it covers | Extra claims | Records needed | Best fit |

|---|---|---|---|---|---|

| Fixed Rate Method | Hours worked from home × $0.70 | Electricity, phone, internet, stationery, computer consumables | Some equipment decline in value and repairs may still be claimed separately | Full-year hour log + proof you paid for covered cost types | People who want a simpler claim |

| Actual Cost Method | Claim the work-related share of each expense | Running costs based on what you spent | Equipment decline in value can be claimed with work-use split | Receipts, invoices, usage records, and apportionment records | People with higher costs and stronger records |

Bottom line: one method gives you less admin; the other gives you a claim that may be closer to your actual spend. I’d choose based on your hours, your bills, your equipment, and how well you’ve tracked everything during the year. If you need help deciding, a tax agent can review your records to ensure you maximize your refund.

1. ATO Fixed Rate Method

The fixed rate method rolls a group of common running costs into one hourly claim, so you don't need to work through each bill line by line. You simply multiply your total work-from-home hours by $0.70 per hour. The catch is simple: you can't claim those bundled costs again as separate deductions.

Expenses covered

This rate already covers electricity, phone, internet, stationery and computer consumables. So those can't be claimed separately. Costs outside the rate, such as depreciation of office furniture or equipment, plus repairs to those assets, may still be claimed separately under this method.

The main job here is proving how many hours you worked from home.

Eligibility and fit

Sole traders and employees who work from home can use this method if the hours are work-related. It's a good fit for people with steady home-working hours and fairly simple running costs, especially if they don't want to split utilities and smaller items across work and personal use.

Record keeping

Since 1 July 2022, you need a record of your actual hours worked from home for the full year. A diary, timesheet, roster or similar log that covers the full income year will do the job. You also need at least one document showing you paid for each type of running cost covered by the rate, such as a phone bill or electricity bill.

That hour log is what your final deduction rests on.

Deduction potential

Your deduction is worked out by multiplying your recorded work-from-home hours by the fixed hourly rate. Put simply, the more hours you can back up with records, the larger your claim can be.

2. ATO Actual Cost Method

The actual cost method lets you claim the work-related share of each expense instead of using a flat hourly rate. In plain terms, you’re working from what you actually spent. That can make your claim more precise, but it also means more paperwork. Each expense must be incurred to earn assessable income.

Expenses covered

You can claim the decline in value of work-related equipment, on top of the running costs already covered in the introduction. If you use something for both work and private purposes, you need to split the expense on a reasonable basis.

Eligibility and fit

This method tends to suit people with higher work-from-home costs who are also good at keeping detailed records. It may work well if you have:

- higher electricity or internet costs

- depreciating equipment

- a high percentage of work use

That’s why this method can appeal to people whose home setup costs more than the standard fixed rate would cover.

Record keeping

The actual cost method needs more detailed records. Keep receipts and invoices, along with a diary or usage log for mixed-use costs. For assets, keep purchase records and use one consistent apportionment method to work out the work-related share.

That extra detail is often the deciding factor when choosing between this method and the fixed rate method.

Deduction potential

Your claim can be higher than the fixed rate method if your work-related costs are high enough. The catch is simple: more detail, more records.

How the Two Methods Compare in Practice

The main issue isn’t whether these methods exist. It’s which one lines up best with your records and how much you’ve actually spent.

The fixed rate method gives you less admin. The trade-off is that it also gives you less detail. The actual cost method is the opposite: more work, but a closer match to what you paid.

Expenses Covered Under Each Method

With the fixed rate method, the hourly rate already covers electricity, phone, internet, stationery and computer consumables. That means you can’t claim those again as separate deductions.

| Expense | Fixed Rate Method | Actual Cost Method |

|---|---|---|

| Electricity and gas | Included in rate | Claimed separately |

| Phone and internet | Included in rate | Claimed separately |

| Stationery and computer consumables | Included in rate | Claimed separately |

| Decline in value of equipment | Not included | Claimed separately |

That one difference has a big effect on both your paperwork and the size of your claim.

Who Each Method Suits

In day-to-day use, the better option depends on how involved your home office setup is.

The actual cost method suits taxpayers with a dedicated workspace, higher equipment costs, or changes made to the home for work use.

If your setup is fairly plain and your expenses aren’t all that high, the fixed rate method will often be the easier path.

Record Keeping and Apportionment

The fixed rate method needs a record of your total work-from-home hours. A diary, timesheet or roster is enough.

The actual cost method needs much more. You’ll need receipts and invoices for each expense, plus a clear and steady way to work out the work-related share of anything used for both work and private purposes. The ATO requires a fair and reasonable apportionment. For mixed-use items, any incidental private benefit must be excluded.

Put simply: if an item does double duty, you can only claim the work part.

Deduction Outcomes in Typical Situations

The fixed rate method tends to work best when your work-from-home costs are ordinary and your records are simple.

The actual cost method tends to work better when your costs are higher and your records can back up the split between work and private use.

Pros and Cons of Each Method

Here’s the side-by-side view on claim size, record burden and overall fit.

| Fixed Rate Method | Actual Cost Method | |

|---|---|---|

| Pros | Simpler to calculate; simple hourly calculation; fewer expense splits | Can produce a higher deduction if actual expenses are high |

| Cons | May result in a lower deduction than your actual running costs | Complex record-keeping; requires receipts, invoices, usage logs and depreciation records |

| Best for | Individuals with modest home office expenses or those prioritising ease of lodgement | Sole traders with dedicated home offices, high utility costs, or expensive equipment |

| Watch-outs | Must keep a full-year record of hours worked | Must apportion private and work use correctly; poor records can lead to reduced or denied claims |

The trade-off is pretty clear: less admin vs a claim that more closely reflects what you spent.

If your home office costs are modest and you want the easier path, the fixed rate method will often make more sense. If your costs are higher and your records are in good shape, the actual cost method may give you a bigger deduction.

For larger claims, it can help to get a registered tax agent or bookkeeper involved. They can sort out receipts, Xero coding and support records before lodgement.

Conclusion

The choice comes down to simplicity versus precision. Neither method wins every time.

Use the fixed rate method when your claim is fairly simple. Go with the actual cost method when your costs are higher and you have the records to back them up.

Keep your records during the year. End-of-year estimates are weak and can fall over fast. What matters most is your expense level, the quality of your records, and how you apportion the claim.

If the claim gets tricky, it’s smart to have a tax agent review your apportionment before lodging your small business tax return.

FAQs

Which method gives the bigger deduction?

There’s no one-size-fits-all method that always gives you a bigger deduction. The better option comes down to your home office costs and how well you’ve kept your records.

The actual cost method can lead to a larger claim if your out-of-pocket expenses are on the higher side. The fixed rate method is easier to work out and usually takes less effort at tax time.

A tax agent at The Priory Books and Tax can help you figure out which method fits your situation.

Can I switch methods each tax year?

Yes. In most cases, you can choose the home office claim method that suits your situation for each tax year. You’re not stuck with the same method forever.

The main thing is simple: keep the right records for the method you use in that year.

What records will the ATO accept?

The ATO will accept records that show you incurred the expenses and how they relate to your work. That can include receipts, invoices, or other written evidence for actual costs, along with records of your hours worked from home, such as a diary, timesheets, or rosters.

Make sure your records clearly separate work-related use from private expenses.

Related Blog Posts

Related: Restaurant Tracking Categories in Xero.